The system we have today is actually broken, only we haven't quite recognized it yet. And so we need a new one, and this is the time to do it, while the markets haven't quite figured it out yet.

The preceding were the words of a billionaire more than a year ago. The following are the words of a Federal Reserve Bank president from just a couple days ago (emphasis mine)… Should the debate that is happening privately remain hidden from the public eye…? Is the nation somehow better served by giving the public the impression that the entire [Fed] is in agreement…? A gold standard that forces countries to back their currency reserves with bullion is a legitimate monetary system.

This being the "year of the RPG" here at FOFOA, I thought it would be a good idea to keep an eye on how gold is acting as "a key reference point to allow people to assess the relations between different currencies" (to quote the head of the World Bank) throughout the coming year.

In order for the limited and stable quantity of above-ground physical gold to perform this important international function effectively, it will ultimately trade independent from the current network of bookkeeping derivatives that assume gold ownership through a counterparty's gold liability (receivables, futures, options, forwards, ETF shares, etc.). Such contractual obligations do not represent a stable and credible quantity like the physical gold itself does, and therefore they make a poor and distorted pricing benchmark.

_________________________________________________________

Sidebar:

More than 10 years ago FOA blew the whistle on the inevitable failure and subsequent dénouement of this distorted benchmark. From my post 100:1:

FOA (05/06/00; 16:45:21MT - usagold.com msg#20)

For Your Eyes Only!

By holding physical gold you are owning a super leveraged "derivative" that will be exchangeable against the value of real things at a par level lost to the minds of most investors. Today, physical gold purchased in dollar values is discounting its worth by perhaps 100 times. For us PGAs (physical gold advocates), that is a leverage worth "playing the physical game for"! (smile)

… Throw in the fact that the earth will not give up all its gold any time soon, present world gold holdings in reserve currency today must rise in value at least 100 times to match what assets now exist. On top of that add in the fact that dollar gold will go sky high just to equal past dollar creation (as the dollar fails) and one can see where physical gold is "the play" in modern times. Forget stocks, business valuations, land or currencies: physical gold is the wealth for the next generation.

FOA (10/9/01; 10:05:48MT - usagold.com msg#117)

Lost in all the confusion is the distinction between investing in the price of gold and investing in gold itself. Perhaps 90% of all the investing in today's worldwide, dollar settled, gold market is done in this first way mentioned. Yes, the market is structured, contractually, to settle in gold. However, in practice, in norm, and in past legal precedent, it is accepted that paper gold trading is meant to only capture the price movements in gold while ceding, what could be, controlling physical trades and their price setting function to other market areas.

Obviously, this is the way it all started, years ago, with the physical trading and its fundamentals dominating the lesser paper trading. But the market evolved with the paper contractual trading becoming 100 or more times the size of the physical side. But everyone already knows all this, right?

From a Friend

Ref: "In other words, the current price of gold means that you are buying a slice of the world’s gold supply with a proportionately smaller slice of the world’s money. You can currently buy x% of the world’s gold with y% of the world’s money, where x is much bigger than y. When gold will become the unit of account of the world’s wealth, you will find yourself able to claim a much bigger slice of that wealth than you would have been able to do with fiat money before the collapse."

This means that CBs and gold-clearinghouse BIS must attach a much higher VALUE to the gold they exchange (redistribute) than the public (visible) goldprice(s).

Note the difference between Value and price. The price is for bookkeeping purposes. The Value is for wealth reserve purposes.

That's why a private person cannot buy goldmetal directly from any CB (or BIS/IMF) ! We are not allowed to know how CB gold " flows " (and is valued in the inner circle). We have no idea how bullion banks intermediaries let goldmetal circulate from goldmine to state and private entities.

We are not allowed to know how the CB/IMF gold auctions really happen. How can we possibly verify the goldprices that are publicised ? Who are the receivers of the WAG gold redistribution ?

So much CB gold-Action and so little transparency. WHY !?

Because of Big difference between price and Value !?

_________________________________________________________

Of course today this is not yet the case. When we say "the gold market" today we mean all of the above paper contracts plus the gold itself. But that doesn't mean that everyone in the world views gold in this same way. They don't. It is really only us in the West, encouraged by the cheerleaders on CNBC, that carry this laughably optimistic view of counterparty trustworthiness when it comes to gold. Other more "giant" and less "Western thinking" entities around the world have quietly taken steps to prepare for the future.

Certain "giant entities" are, and have been for more than a decade, marking their physical-only gold assets to the market price of "paper gold" the whole time it has been rising from its low of around $250 per ounce. This doesn't seem like a very big deal to the Western mindset that can't see the difference between "counterparty gold" and "counterparty-free gold," but it is actually quite significant given the history of metal used as currency.

In the past, whenever any metal has been used in a monetary function during the presence of a government or monetary authority, the metal itself has endured a trade-value distortion that is always in conflict with the market forces present at that time. This market distortion is what has melded metal into money during these past systems. Not its free market floating value, but just the opposite; the suppression of free market forces on that specific monetary metal.

For example, you can stamp a metal into coins and declare that your coin form of the metal is of higher value than uncoined metal in payments you make and those made back to you. This is a way to overvalue a portion of a commodity metal's above-ground supply to your advantage. You are marking your specially stamped metal above the rest of the market metal, or "marking it to your model."

But over time, this method of monetizing a metal has always run into the same problem. The market for uncoined commodity metal always seems to catch up and overtake the face value of your coined metal and you are forced to dilute your currency into ultimate collapse, occasionally on a civilizational scale.

So then you might declare that all of a certain metal, coined or uncoined, is the monetary base or standardized unit of another money that you can print very easily. This method becomes more of a confidence trick because you are attempting to undervalue that metal (the entire quantity of it) out in the free market, relative to the easy money that you can print.

In order to support this confidence trick you must become both the buyer and seller of last resort of both your metal and your easy money. You must buy your easy money back with your metal and vice versa. This trick can last until you run out of one or the other. Of course, you need never run out of the easy money you can print, so that's not the real danger in this con.

In a sense, or perhaps in essence, today's paper gold market is not very different from this second monetary scheme. The banks that create paper contracts for "counterparty gold" by simply writing them become the buyer and seller of last resort for both their own paper promises and real physical gold. This can continue until one or the other runs out. But again, you are marking a metal to your model of a marketplace that includes both the metal and your paper creation, be it dollars or "counterparty gold."

There are many variations of these schemes in which the value of various metals had to be distorted by authorities in order for them to fulfill any useful monetary function. And there are also many examples where monetary authorities were forced to adjust or abandon their preferred money to avoid drowning in the unstoppable tide that is the market force. Like France in the 1870s abandoning its planned return to bimetallism in order to avoid having to spend its gold buying up all the excess silver in the world. [1] Or Sweden's successful move in 1916, closing its mint to the previously free coinage of all gold in order to levitate the value of Sweden's coined gold back above the market price of uncoined gold. [2]

All of these market/monetary shenanigans of the past stand in stark contrast to what is being performed today in broad daylight, once every three months, on the Consolidated Financial Statement of the youngest major monetary authority in the world. Once per quarter, the ECB openly marks the Eurosystem's monetary reserve assets, including the physical gold asset, to the last market price of the previous quarter. This is marked to market (MTM) monetary authority gold in the specific role of reserve asset, aka store of value. And while the implications of this 180 degree shift in any major monetary authority's regard for gold is not widely discussed, it is immensely significant. (See: FOFOA)

So without further ado, let's get to the latest Eurosystem reserve revaluation, just released Wednesday, and see how our RPG (Reference Point Gold) is holding up. First, I will show you how you can follow this on your own, or even go back and check past statements for analysis, or just for fun.

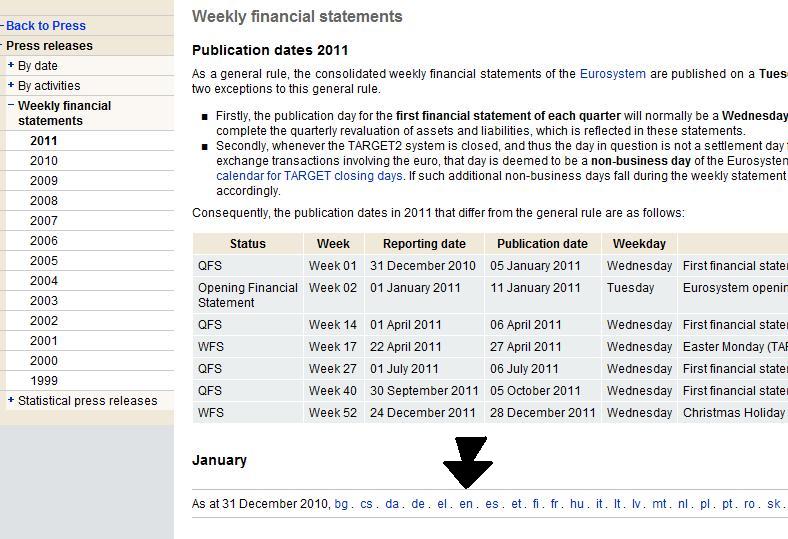

If you click on the following link to the ECB website you will see a description of the "Weekly financial statements" they publish every week:

http://www.ecb.int/press/pr/wfs/2011/html/index.en.html

It reads: "As a general rule, the consolidated weekly financial statements of the Eurosystem are published on a Tuesday, and they relate to the preceding Friday. There are two exceptions to this general rule.

"Firstly, the publication day for the first financial statement of each quarter will normally be a Wednesday (instead of Tuesday) in order to allow more time to complete the quarterly revaluation of assets and liabilities, which is reflected in these statements."

Note the use of the word "consolidated." This means that every line on the statement relates to the entire Eurosystem, not just the ECB. So the gold listed on this form is the consolidated total of the official gold reserves of all its member states. Same for other itemized assets and liabilities. Also note that they only perform the market-based revaluation of assets on every 13th statement (once a quarter). And for these, they allow an extra day, publishing on Wednesday instead of Tuesday. And this being the first week in January, we got the new numbers on Wednesday.

Below the description you'll see a list of the actual publication dates for the quarterly revaluations this year:

To the left you can click on any year going back to the launch of the ECB on Jan. 1, 1999 and review the weekly and quarterly reports from each year:

And down at the bottom, you can click on the language of your choice for today's quarterly statement, "en" for English:

So let's click "en" for English and check out the latest ECB press release, the "Consolidated financial statement of the Eurosystem as at 31 December 2010" or ConFinStat for short. If we scroll down a little we'll come to the actual balance sheet. This lists out all of the Eurosystem's official assets and liabilities, listed in their euro value, the official unit of account in Euroland.

Quantitative changes to this sheet are published every week, but qualitative changes, the line items signifying foreign currency assets and gold, are only revalued into the euro unit of account once per quarter. Just above the balance sheet you'll see the only section that differentiates this quarterly statement from any other weekly statement, the "Quarter-end revaluation of the Eurosystem’s assets and liabilities."

Notice the black arrow pointing to the following:

Gold: EUR 1055.418 per fine oz.

USD: 1.3362 per EUR

JPY: 108.65 per EUR

Special drawing rights: EUR 1.1572 per SDR

These four lines are the "market snapshot" that is taken once every three months, mentioned in my last post. It is a snapshot of the euro's market price as it floats against four different benchmarks or reference points. It is used to calculate the weight of those most valuable line items to any Central Banker, the reserves that cannot be printed and are therefore used to defend and evaluate that which can be printed. This snapshot will be used for the next 90 days.

For comparison, here's the last "snapshot" taken on Oct. 1, 2010:

Gold: EUR 960.580 per fine oz.

USD: 1.3648 per EUR

JPY: 113.68 per EUR

Special drawing rights: EUR 1.1399 per SDR

Right off the bat you should notice an interesting thing. Look at the percentage of the euro's change against the other fiat currencies. 2.1% change against the dollar. 4.6% against the yen. And only 1.5% against the SDR. They are all falling in tandem! Yet there's a 9.9% change against gold over the same time period. What you are witnessing here is the emergence of a true leader, the benchmark or Reference Point par excellence, from the rest of the pack of potential "reference point contenders."

Now let's take a look at the actual balance sheet to see how this Reference Point snapshot is applied. In the image below I have placed the asset side of the previous statement released on Dec. 28 side by side with Wednesday's release.

One distinction I want you to notice is the two columns on the quarterly statement, which I circled. Column "i" is for transactions or quantitative changes from the week before (this is the column that is reported every week), and column "ii" is for the "snapshot-based" adjustments or qualitative changes from the previous week/quarter.

You'll see from the previous statement that there was a net increase of approximately €1 million worth of gold (only around 1,000 ounces) to the Eurosystem stockpile during the week ending on Christmas Eve (possibly delivered by Santa). And in column "i" you'll also see that there was no change to quantity of gold during the week between Christmas and New Year. There was only a "qualitative" change (revaluation) which was reported in column "ii." And that change was +€33 billion for the Eurosystem's 348.1 million ounces (10,827 tonnes) of gold.

The other important thing to note on these ConFinStats is the gradually changing relationship between gold reserves and foreign currency reserves. These are both "hard money" reserves to the ECB because they must be acquired "the old fashioned way," or the "hard" way; they cannot be printed. This is what makes them valuable to any Central Bank. They are what is sometimes used to defend the value of the "easy money" that can be printed. And the qualitative relationship between these two fundamentally different kinds of reserves has been changing for the past 12 years!

As Randy Strauss of USAGold fame so eloquently points out here, "gold’s role has gained musculature from a mere 30.5% proportion to its current dominance now at 67.1%." That means that at the beginning, in 1999, Eurosystem reserves were made up of 69.5% foreign fiat paper and 30.5% gold. Today that has shifted qualitatively to a net foreign paper position of only 32.9% to gold's 67.1%, a virtual flip flop!

And what makes this so significant (and unique) for the euro is the way the ECB measures itself nakedly, transparently, against all competing benchmarks. The ECB valiantly reports ALL foreign holdings in its own unit of account, displaying itself confidently against any and all reference points. Second only to the ECB MTM concept, this is the revolutionary CB practice that other major CBs have yet to adopt. Most CBs still report their dollar holdings in Ben Bernanke's favorite benchmark, the dollar itself, master at the confidence art of self-reference.

Speaking of the dollar, it is difficult to maintain yourself as the global reference point if you are seen to be losing your youthful posture. So let's take a quick look at how an aged major monetary authority (preparing for its 100th birthday party in 2013) deals with this conundrum. It's not as pretty as the spry ECB statement, but here is the Fed's asset report from its latest release, "Factors Affecting Reserve Balances" (just released yesterday):

The salient point here (circled) is what Randy Strauss expounded on in his previously linked piece:

"Meanwhile, due to the woefully outdated paradigm established by the U.S. Congress for gold held by the Treasury Department, the gold reserves of the United States are effectively anemic and bedridden upon the books of The Federal Reserve System, where they exist only in certificate form — valued at a static $42.22/oz., forming a paltry $11 billion stake."

That's right! The Fed doesn't even have actual gold on its balance sheet that can be used as a reference point. It has "gold certificates" issued to it by the U.S. Treasury from the past monetization of U.S. Treasury gold at $42.22/oz. I suppose, technically, if the U.S. Treasury wanted to revalue its gold to the market price today, the proper yet antiquated process would be for the Fed to credit the Treasury's spending account with new dollars representing the difference in price. Today that would be about $355 billion fresh dollars for Congress to spend. Yet there would still be no existing mechanism to automatically account for the new and emerging Reference Point: Gold. Something technical is going to have to change!

But that's not really my concern. That is something for Congress, the Treasury and the Fed to collectively figure out. My concern is simply how this shifting, changing and adjusting international monetary system will affect my balance sheet. And that's why I have put myself on my own personal RPG. I have consolidated my assets. And in doing so, I have favored the genuine article over its lesser reproductions.

What makes me sad, though, is that some of the most studious and longstanding gold bugs, some of the most ardent "honest money" advocates, will apparently be slower to grasp this unfolding system of "RPG/Freegold" than the flocks of Sheeple, or even the Chartalists. Sometimes you've just got to "unlearn" a little past dogma in order to comprehend present reality.

The "silver lining" for them is that, at least, hopefully, they will have some physical gold in their immediate possession so as to participate in the RPG party train. If not, well, hopefully the commodities they invested in will at least rise with inflation and not succumb to the global economy resetting as it adjusts to its newfound lack of a 300 million-strong group of net consumers.

FOA (8/22/01; 05:18:54MT - usagold.com msg#98)

The war between gold and the dollar has been over for a while now. The action, today, is between the dollar and the euro arena and this is what will break the price lock on gold.

.................................................................................

FOA (07/27/01; 15:20:44MT - usagold.com msg#85)

"The Wind Will Blow"

Circulating cash dollars, official metal coinage and other previous fiats, themselves thought of as a final hard payment, were never any more than a known tradable value. A trade credit owed to you as long as one held the money unit. Even with gold backing the dollar unit, money's value was always in its exchange for something else we wanted. Gold values behind these fiats was used to represent some fixed tradable value the money unit stood for; not to be the money unit itself.

.................................................................................

The immovable past structure the dollar is built upon demands its values be defended with complete hyperinflation if necessary. Prior to EMU, there was no other reserve currency that the world could run to. Now, the dollar cannot deflate and take the rest of the world into deflation with it. The tables are turned; deflationary policy will not defend the dollar. Only inflationary policy will. Make no mistake, we are not calling for price inflation to end the dollar's reserve rein! We are calling for "inflationary policy" to dethrone it while said hyperinflation follows.

.................................................................................

The next step will be an orderly exit from dollar use; a somewhat destruction of all dollar gold pricing; and a super price inflation for US dollar assets. We are not at the end my friends, we have just come to the beginning. For physical gold advocates that understand the difference between real wealth and leveraged real wealth, the time arrives when values are reflected with the speed of the wind. Truly, in our time, "The Wind Will Blow".

.................................................................................

Having evolved a dollar reserve money system into a straight debt fiat currency, without gold involvement, the entire dollar function became locked into one basic premise: for the system to survive, its core reserves of debt values had to remain somewhat price stable as the currency inflated relative to GDP. Over the next 30+ years their dollar controllers, the fed and treasury, thought they had a fairly good handle on the system as they managed banking reserve requirements. To their amazement, it turns out today, that digital use demand was the best function that supported their efforts all the while; by increasing the world's use and need for currency. Had they understood this modern economic function early on, they could have somewhat printed the currency outright with almost the same result while arriving at today's destination. They could have let gold float, not to mention they could have skipped a large portion of the debt build up that will now end the dollars timeline.

Most, if not all, of this perspective is only now coming to light as the Euro builds pressure on the dollar. The better architecture of the Euro system is leaving little room to adjust as the US fed must singularly act to inflate their local currency in a historically new and unprecedented fashion. The actual debt machine that built much of America's lifestyle is now going into reverse as it destroys its own currency; one built upon a stable debt system with locked down gold prices.

.................................................................................

Without an international floating gold reserve pricing, to balance against their devaluing debt reserve, the entire dollar banking system can only rely upon extreme dollar inflation to float its accounts. Price inflation will have to be ignored. To this end the group of dollar supporting countries, we refer to as the dollar faction, has locked itself into a box. It must find a way to float gold prices with a gold reserve that only drains away if world gold price rise.

.................................................................................

How far will gold rise? At first blush, foreign dollar assets will not, in any way, return home! They will circulate offshore; either from lack of understanding of the issues, a thought that things will be worked out or from foreign exchange controls aimed at protecting the failing US economy!...

Mini-Sidebar

Exogenous (or exogeneous) (from the Greek words "exo" and "genis", meaning "outside" and "generated") refers to an action or object coming from outside a system. It is the opposite of endogenous, something generated from within the system.

In an economic model, an exogenous change is one that comes from outside the model and is unexplained by the model. For example, in the simple supply and demand model, a change in consumer tastes or preferences is unexplained by the model and also leads to endogenous changes in demand that lead to changes in the equilibrium price. Similarly, a change in the consumer's income is given outside the model. Put another way, an exogenous change involves an alteration of a variable that is autonomous, i.e., unaffected by the workings of the model.

...These reserves will circulate until their gross exchange value simulates a figure that can be reasonably expected to "buy something" within the US; ten cents on the dollar could be a guess? However, keep in mind that the fed will be printing like mad, local prices will be soaring and no one will be chasing dollars like they do today. I expect that physical gold trading, within the US, will follow far behind foreign trading for a time. Perhaps a $5,000 to $15,000 ratio will be a thought as dollars within the US will be worth more than outside. Still, the relative value of physical gold will eventually converge as a trading standard is reached.

.................................................................................

Sincerely,

FOFOA

[1] Mundell - The International Monetary System in the 21st Century: Could Gold Make a Comeback?

[2] Hayek - A Free-Market Monetary System

227 comments:

«Oldest ‹Older 201 – 227 of 227Since Blondie's linked post isn't showing for some reason, I thought I would post a link to it as well as my last comment did show...

http://flowofvalue.blogspot.com/2010/10/why-tax-freegold_5446.html

In fairness to Daniel Amerman, his out-of-box alternate solutions do work. Although gold is not the center of his universe, it is one part of a flexible, diversified approach. The centerpiece is the inevitable destruction of the purchasing power of dollar-debt, incurred only for purchasing income-producing assets (apartment buildings, agri-land, energy). The nominal dollar debt gets wiped out by (hyper)inflation; you get to keep the asset, and legally avoid all taxes. Brilliant and unique. Think long and hard on his latest article, ignore it at your likely peril. Daniel Amerman's professional credentials, original thinking, practical solutions and integrity are all top notch. On his site, Daniel does offer an excellent, TOTALLY FREE series of really valuable articles. I have attended two of his workshops and bought the entire DVD set:Some of the best educational money I ever spent - along with this FOFOA blog,of course.

Mystrybox - it's a big world out there. People need to start thinking outside the box(The West) Are all of the "outside" $'s going to be confiscated and if so how? What will they be replaced with? Will they be cancelled out? How would that effect $ credits inside the U.S? Would the world stand for that?

What about all of cash societies where plastic hasn't caught on yet? Would somebody voluntarily go from storing savings in gold and using currencies in transaction to using plastic for everything? I don't think so but I'm just asking questions here.

Can a traveler to Asia who normally carries Euro's or $'s exchange his plastic based credits for cash in Asia?? Maybe, maybe not but it's something to think about. What about the foreign banks who were going to settle up in paper dollars? Do they roll over and take in digits? Will the U.S allow them to spend these digits inside the U.S and if not do you think anyone will accept these digits in the East for their production, goods, or commodities?

The entire world is effected by the $ reserve system but a change to plastic would not go over so well. Step outside of your mysterybox and take a look at the world.

@DP,

How is it that you can see my unpublished comment, which is currently in FOFOA's Blogger spambox?

@ Laszlo,

I agree entirely; Amerman is top notch, and I do not doubt his integrity. I have read all his free articles published over the last couple of years, and benefitted from his unique approach.

His frame of reference however does not include Freegold, but rather the extrapolation of the status quo (if you know what I mean). I see Freegold as an organic market based response (invisible hand) to the USD debt load and reserve status breakdown, thus negating Amerman's gold tax ideas from my perspective, but not his methodology.

Just my opinion, of course.

DP

Unfortunately, if you do not have any paperwork to show your purchase price, the government assumes one of two things--you owe tax on the full value, and/or you stole the stuff.

They have no problem whatsoever figuring out what your basis is--it is zero!

Jim Sinclair’s Commentary on the Forbes article:

Forbes has got it right. Gold is not going to take a 1980 flop. Gold is going to $1650 and above.

In time a virtual world currency as an average of many currencies tied to gold via a large measure of world M3 will occur. It will not be convertible, however it will be accepted as an alarm set in a monetary concept.

That has been lacking since currencies went to float in the marketplace against each other.

Gold will trade as a pendulum around the price of gold at the inception of this monetary plan. The dollar will remain in reserves of many countries primarily because they are simply stuck.

Sounds like the one time revaluation to me and an almost Freegold. FOFOA and all, any thoughts on Sinclairs assertion?

DP, what you think the government will just say, oh well he doesn't know his cost basis so we'll let him pay nothing? If you can't prove what you got it at you'll have to pay as if your cost basis was zero.

Blondie, right Amerman sells DVDs and such with solutions to the problems he sees. But he's still got a lot of very good free articles. If you read his free material it's not difficult to know generally what his "solutions" must be that he sells. But yeah if it morally bothers you when people try to make a living off what they know then you might avoid his articles. Capitalism isn't for everyone.

What I'm saying is that I choose to buy gold as sovereigns because they are legal tender and therefore are not subject to Capital Gains tax in the UK. This is unlikely to change. You likely have similar legal tender coins where you live too.

DP,

Suppose you received your gold coin as a "gift" (or claim as such): Just shot yourself in the foot, as your tax basis is now simply zero. For US persons, the entire sales proceeds would be considered "profit", currently with 28% going to Uncle Sugar alone, plus more to your near-bankrupt state, like Illinois at the new 5%. Saving your receipt would actually save you on taxes. Otherwise, as a lucky US person, you risk enjoying your FreeGold from behind steel bars. Unless, you are willing to proactively move your ass and assets to Another country that lets you settle, plus gives/sells you citizenship; then and only then can you expatriate and be rid of your obligations to Uncle Sugar. Choose your love - but then, you'll have to love your choice. When push comes to shove, your newly-adapted country might not treat you much better than Uncle Sugar. The devil is in the details. Might want to check out both Daniel Amerman and Sovereign Society. None of these comments are advice: Think long and hard, then dyodd.

GOLD FREAK said "Mystrybox - it's a big world out there. People need to start thinking outside the box(The West) Are all of the "outside" $'s going to be confiscated and if so how?"

Just like the article said. One day we're told that cash will be worthless at some point in the future and all cash needs to be deposited into an electronic account before that point. After that point the US is cashless. It's the same thing that happened with gold confiscation. One day bang, gold is illegal... and surprisingly not much changes for most people in day to day life.

"What will they be replaced with?"

It's still dollars, just electronic... accessed ONLY via debit cards, credit cards, and other identification systems they come up with. Not much different than today for most people.

"How would that effect $ credits inside the U.S? Would the world stand for that?"

The same way as today--with dollars. Just no physical cash. All transactions electronically handled and tracked.

"What about all of cash societies where plastic hasn't caught on yet?"

Obviously our local laws won't effect other countries just like our gold confiscation only happened here.

"Can a traveler to Asia who normally carries Euro's or $'s exchange his plastic based credits for cash in Asia?? Maybe, maybe not but it's something to think about. What about the foreign banks who were going to settle up in paper dollars? Do they roll over and take in digits? Will the U.S allow them to spend these digits inside the U.S and if not do you think anyone will accept these digits in the East for their production, goods, or commodities?"

The bulk of dollars outside the US are already electronic. However if required cash dollars might still be legal outside the US just as gold dollars were legal outside the US after confiscation. China had different currencies for outsiders vs their population when I was last there though that might be changed now.

I think it's you who needs to think about this deeper. And read the article too as by your comments it doesn't seem that you did.

Best,

--MystryBox

mystrybox:

Amerman's article about a control-freak set of governments is indeed something to give pause.

However, there are many people today who have never used a piece of plastic. My mother and grandmother, for example. I would think this sort of change would need to be announced a couple years ahead of time, like they did when TVs went digital.

Another major issue is the system itself. Much, if not all electronic equipment can be destroyed by radiation created by solar flares and/or air-exploded nuclear bombs. This would be a major, major problem even today, but even more mind-boggling and deadly if there was no back-up (cash) system.

That's not to say that, if backed against a wall, the power-elite might not try it, future be damned. If they feel threatened, they will try anything and everything to retain power and control.

@Blondie: If I told you that, you'd know as well! :D

(I get them all via Gmail on my Android, spam or no, it seems)

MysteryBox,

Unless you buy at least the two gold DVDs, you would never happen upon Amerman's professional, practical and legal solutions. I took the free course, the paid workshops and bought the DVDs.Well worth of the price.

Laszlo,

The problem I see with the solutions implied by Amerman's free articles is they would involve buying gold (and perhaps real estate) with leverage. Leveraged strategies are highly risky and can end up very badly if things don't go exactly as expected.

I mean what if you leverage buy gold today and somehow the government bends some rules and manages somehow to smash the gold price significantly, even if only temporarily? A leveraged strategy will not survive.

Emotionally most people who are leveraged won't be able to handle even a significant pullback of the completely natural kind that occasionally happens in a bull market and will exit with massive losses at the exact wrong time.

It's difficult enough to invest properly without leverage. So I don't see his strategies (or at least what I suspect his strategies are) as being practical.

Best,

MystryBox

So, none of you have any comments about the points well made in Blondie's article?

I'm surprised, and a little disappointed. :)

MysteryBox,

I absolutely agree with you on the dangers of leverage. Per Amerman, the only leverage would be on income-producing assets (like apartments or farmland you lease to a farmer, maybe wind turbine or gas/mineral rights royalties, that you get cashflow, perhaps even subsidies). The only loan would be a government-subsidized, preferential, low% mortgage on apartments, etc., as there is no longer any private mortgage market in the US. As to your gold: You must buy it preferably without any loan (so you can fondle it and keep it safe from thieves). If anything, your gold purchases could be perhaps judiciously assisted by an existing home equity loan, with proceeds spent discretely, so you can still fondle it. If.. eh, I mean, when the grand FreeGold revaluation actually happens, you will not need a huge number of ounces to make all the difference relative to your neighbors. Afterward, you can pay off your debts with a couple of pennies on the hyper-inflated original loan principal. Then after the world returns to some kind of normalcy, you pull the magic trick of pulling your equity out of your apartments, completely, legally tax-free, by refinancing. No, the world will not end. Yes, you pull your entire equity tax free. Yes, 100% legal. Yes, Amerman is 100% genius. Then you buy the DOW for under one ounce of gold, maybe far less, post-FreeGold-revaluation. Live happily ever after off widely diversified blue chip dividends, some from China. Who says you can't eat your gold? On the gold portion, you either feed the tax monster, or you may be able to barter or borrow against it. My crystal ball gets a bit cloudy there. :-)

MysteryBox,

The mortgage on the apartment or other income-producing asset would be very conservative, say 40% to 65% LTV, (loan-to-value) to withstand the storms ahead, including continued declining valuations. Your fully paid for physical stash of gold in hand would provide buffer. I was totally shocked to learn the that you need not buy anywhere near the bottom of the real estate market, not by a long shot. The loan rates, income/expense on the asset are far more important. Used to be hugely counter-intuitive, until Amerman's workshop or DVDs enlightened me. The free email series are insightful, but the real deal is the for-fee part. Can't blame him, can you? Daniel provides great value,at twice the price.

As Blondie said, I think the problem is that Amerman's idea extrapolates too much of the past into the post-Freegold future. As I've said before, I don't think you'll see real estate prices rocket up with gold, so extracting equity probably won't be on the menu IMHO.

Easily paying down your old mortgage $debts with massively revalued gold (and only gold), yes that I can see.

MysteryBox,

All my prior comments were based on US situation. Long legal history suggests a well-established respect for / adherence to the letter of contract law stipulating, in nominal dollar terms, with no adjustments for purchasing power parity. None. The civil and tax laws are blind to the actual purchasing power shifts from the original contract, like mortgages, bonds, insurance, annuities. Gullible buyers of paper promises, of toxic fiat-based waste, beware: you face potential imminent total wipe-out: You will not be rescued to any extent(unless you are TBTF). Meaning, positioned properly, in the US, you have a far better chance of fully benefiting from hyperinflation destroying the purchasing power of your mortgage obligation. On the contrary, in continental Europe, based on Napoleonic Code legal tradition, some sort of reluctant, unpredictable equitable adjustment has been the historical norm. This included Weimar Germany, France, Hungary (repeatedly)and Austria (in the 1920s), where the creditors were eventually able to recoup some small portion - the flip side being, debtor's debts were partially restored, as opposed to total wipe-out. Very partially, so still, debtors win by a large margin. But savers in fiat, bonds and annuities suffer near-total, devastating losses. Gold - Get some. Who said the US was the worst of all places? It just depends how you position yourself. For US debtors, there is long history of relatively easy relief. It started with "no debtor's prisons" in the Land of the Free. Still true, to considerable extent. US/dollar creditors have always been punished for their ignorance and complacency (hope Bank of China personnel are not reading this - I still need time to buy more gold). The US Sheeple still cannot believe Weimar Germany can happen, without notice. Time will tell.

Gentlemen and Gentle Ladies, place your bets. Failing to get gold while you can, is a bet on the status quo.

DP,

True, Amerman does not get the FreeGold paradigm - but he made tremendous progress over the years. By the way, the apartments or farmland are NOT a play on nominal price appreciation at all, nor is it about on reselling for paper dollar profits, ever. That is not his paradigm. Amerman's mortgaged asset plays are just possible, practical means to the end, which is the complete destruction of your mortgage, you ending up with tangible assets, free of debt, with then-current income (cash flow) from the asset, in the future fiat. After all, we will always have fiat, realistically and even hopefully - alongside FreeGold. Amerman's asset is secondary in the strategy: It is needed to get the mortgage, it is the enabling, tax-advantaged dollar-short position. The asset only needs to partially maintain some meaningful purchasing power, relative to fiat, the income is there to carry the mortgage payments and expenses. I buy and hold fully paid physical gold as the one-time "grand revaluation FreeGold" play. For me, two separate plays. Amerman for tax-advantaged diversification, after you reach your capacity to accumulate fully paid physical gold positions, the prime objective of most of us on this blog. Secondarily, I suggest we would be wise to think about how we get from "here and now" to post-revaluation FreeGold, without losing out on the way to leverage, taxman or jailers. Important details, I think. Would A/FOA not encourage us to consider possible trails? I think Amerman provides a valuable fractal option for "extra credit", if you are done with your prime assignment already. In his ways, Amerman is also out of the conventional box, like we are in our ways. No, he is not your source of FreeGold wisdom, of course. Perhaps this is also a holographic universe, not just fractal? One does not necessarily invalidate the other.

Yes, FOFOA, I got the message.

I concluded my December 10th, 2010 "Swiss-bank gold-account - custodial/safekeeping vs. claim account"-post on my "HONEST MONEY"-blog concerning a client of a Swiss bank who could not get hold of the gold he (bought and) stored there as follows:

If the accounts involved are "claim accounts", the stories are not important. The only importance of the stories is then that the storage fees were unduly paid and should be reimbursed to the investor.

However, if the accounts are "custodial accounts" and/or "safekeeping accounts", there may be a little problem of contractual liability of the banks involved.

The storage-fee issue is irrelevant to determine the banks’ contractual liability.

What matters is the kind of metal-account the investor held at the bank. (1)

By raising the issue of the contractual liability of the bank, I implicitly admitted that the bank was a counterparty.

You are stressing in your post above that only the West, encouraged by the cheerleaders on CNBC, carries a laughably optimistic view of counterparty trustworthiness when it comes to gold.

Later in your post, you write, concerning the fact that the Fed doesn't even have actual gold on its balance sheet that can be used as a reference point, that something technical is going to have to change.

And you continue:

QUOTE

Of course today this is not yet the case. What makes me sad, though, is that some of the most studious and longstanding gold bugs, some of the most ardent "HONEST MONEY" advocates, will apparently be slower to grasp this unfolding system of "RPG/Freegold" than the flocks of Sheeple, or even the Chartalists. Sometimes you've just got to "unlearn" a little past dogma in order to comprehend present reality. [emphasis mine]

UNQUOTE

This paragraph is immediately followed by this one:

QUOTE

The "silver lining" for them is that, at least, hopefully, they will have some physical gold in their IMMEDIATE POSSESSION so as to participate in the RPG party train. If not, well, hopefully the commodities they invested in will at least rise with inflation and not succumb to the global economy resetting as it adjusts to its newfound lack of a 300 million-strong group of net consumers. [emphasis mine]

UNQUOTE

Yes, I may have been right in saying that what legally matters or what matters (or will matter) in law (or in a law court) is the kind of contract the client concluded with the bank,.

But if the gold is not in the immediate possession of the bank,

if the gold is not actually stored at the bank or has not actually been stored by the bank,

then the bank will simply be bankrupted by Freegold

and the client has no way to get (the value of) his goldmetal back.

No [bank] can indeed withstand the pressure to print more receipts than it has gold in reserve. (2)

NOTES

(1)

Swiss-bank gold-account - custodial/safekeeping vs. claim account

Posted by Ivo Cerckel on December 10th, 2010

http://bphouse.com/honest_money/2010/12/10/swiss-bank-gold-account-custodialsafekeeping-vs-claim-account/

(2)

Roland Leuschel and Claus Vogt, "Das Greenspan Dossier, Wie die US-Notenbank das Weltwährungssystem gefährdet. Oder: Inflation um jeden Preis", www.finanzbuchverlag.de, 2006, 3rd ed., p. 300

Yes, FOFOA, I got the message.

I concluded my December 10th, 2010 "Swiss-bank gold-account - custodial/safekeeping vs. claim account"-post on my "HONEST MONEY"-blog concerning a client of a Swiss bank who could not get hold of the gold he (bought and) stored there as follows:

If the accounts involved are "claim accounts", the stories are not important. The only importance of the stories is then that the storage fees were unduly paid and should be reimbursed to the investor.

However, if the accounts are "custodial accounts" and/or "safekeeping accounts", there may be a little problem of contractual liability of the banks involved.

The storage-fee issue is irrelevant to determine the banks’ contractual liability.

What matters is the kind of metal-account the investor held at the bank. (1)

By raising the issue of the contractual liability of the bank, I implicitly admitted that the bank was a counterparty.

You are stressing in your post above that only the West, encouraged by the cheerleaders on CNBC, carries a laughably optimistic view of counterparty trustworthiness when it comes to gold.

Later in your post, you write, concerning the fact that the Fed doesn't even have actual gold on its balance sheet that can be used as a reference point, that something technical is going to have to change.

And you continue:

QUOTE

Of course today this is not yet the case. What makes me sad, though, is that some of the most studious and longstanding gold bugs, some of the most ardent "HONEST MONEY" advocates, will apparently be slower to grasp this unfolding system of "RPG/Freegold" than the flocks of Sheeple, or even the Chartalists. Sometimes you've just got to "unlearn" a little past dogma in order to comprehend present reality. [emphasis mine]

UNQUOTE

This paragraph is immediately followed by this one:

QUOTE

The "silver lining" for them is that, at least, hopefully, they will have some physical gold in their IMMEDIATE POSSESSION so as to participate in the RPG party train. If not, well, hopefully the commodities they invested in will at least rise with inflation and not succumb to the global economy resetting as it adjusts to its newfound lack of a 300 million-strong group of net consumers. [emphasis mine]

UNQUOTE

Yes, I may have been right in saying that what legally matters or what matters (or will matter) in law (or in a law court) is the kind of contract the client concluded with the bank,.

But if the gold is not in the immediate possession of the bank,

if the gold is not actually stored at the bank or has not actually been stored by the bank,

then the bank will simply be bankrupted by Freegold

and the client has no way to get (the value of) his goldmetal back.

No [bank] can indeed withstand the pressure to print more receipts than it has gold in reserve. (2)

NOTES

(1)

Swiss-bank gold-account - custodial/safekeeping vs. claim account

Posted by Ivo Cerckel on December 10th, 2010

http://bphouse.com/honest_money/2010/12/10/swiss-bank-gold-account-custodialsafekeeping-vs-claim-account/

(2)

Roland Leuschel and Claus Vogt, "Das Greenspan Dossier, Wie die US-Notenbank das Weltwährungssystem gefährdet. Oder: Inflation um jeden Preis", www.finanzbuchverlag.de, 2006, 3rd ed., p. 300

Wendy,

We are OK where we are. Thank you for asking.

Lots of grief in the northern part of Australia. The majority of the fatalities were in one area struck by a flash flood. I hear it was so sudden people could not get out of harm's way. Evacuations commenced elsewhere as soon as the threat became visible. The loss of life will prove to be very, very small.

The floods are a huge natural disaster but we have a long history of fire, floods etc here. So disaster response is highly effective.

Thankfully this will not be a re-run of post-Katrina New Orleans. The armed forces, private citizens and governments are fully engaged in emergency response and, as of today (our time), the clean up, repair and rebuild phase.

After the tsunami in Indonesia and SE Asia Australia pleged $1 billion in aid. The fundraising has commenced and people are volunteering and will soon be donating in droves if history is any guide.

DP (and Blondie)

This is the paragraph in Bondie's post that leapt off the page at me:

"The profits from this productive use of capital soundly invested would supply a tax base many orders of magnitude larger and for much longer than any possible tax on gold.

I'm an agnostic on this issue of taxing gold after the transition. I think governments are capable of monumental stupidity. However in this case they will have several role models to learn from. I would include the EU, India and China on this list.

The "No" case is very strong but the "Yes" case cannot be disproven at present IMVHO.

PS. Blondie, I think you are doing some really fine work at your blog and in the comments I stumble across in the blogosphere.

I get how there's a problem with the world trying to store all their savings in the form of "American promises for more savings tomorrow", or American debt, but why is there only option to shift to gold as a store of value, instead of storing their savings in the debt of their own domestic currencies? Thinking further, what would be the problem with the world to also start saving more and more of their savings in the form of Chinese promises? In yuan debt that is backed by the productive capacity of the largest creditor nation on earth?

Cheers

Post a Comment

Comments are set on moderate, so they may or may not get through.